Surprise! You Have Taxes Due!

Did you have a surprise tax bill when you filed your return this year? There are a variety of reasons this can happen. Perhaps you take distributions from a retirement account and the amount withheld isn’t sufficient to cover your tax liability from the withdrawal. You received a K1 from a partnership or S-Corp Or, like many people most recently, you’ve started a new business and you’re filing a Schedule C. There are many more reasons, but if the fact that you owe this year is a singular event, it could be the result of recent legislation and not necessarily something that will affect future years’ tax returns. If in doubt, I recommend using the Withholding Estimator at IRS.gov. This will help you plan for any withholding deficiencies ahead of tax season and can even help you complete an updated W4 for submitting to your company’s Human Resources department.

If, however, your shiny new tax bill is the result of a new business, or K1, you should consider filing estimated tax payments each quarter, starting April 18th. You see, the IRS tax system is a pay-as-you-go system. They don’t want you to owe them large amounts of money at the end of the year any more than you do. In fact, they tack on penalties and interest to discourage you from doing so.

There are two ways to estimate your taxes for the coming year. The first is to take your current year tax liability – the whole amount, not just the amount due – and plan to pay 90% of that over the four quarters. This is okay, if your business revenue is the same year after year and you don’t expect any new growth, but I doubt it applies to many of us.

The second method requires some consideration and planning on your part as a business owner. You’ll need to consider what you intend to earn in your business for the year. How you determine that amount is a topic for another day, but still very necessary. Take the net amount of those earnings (Revenue – Expenses) and then start figuring your tax liability.

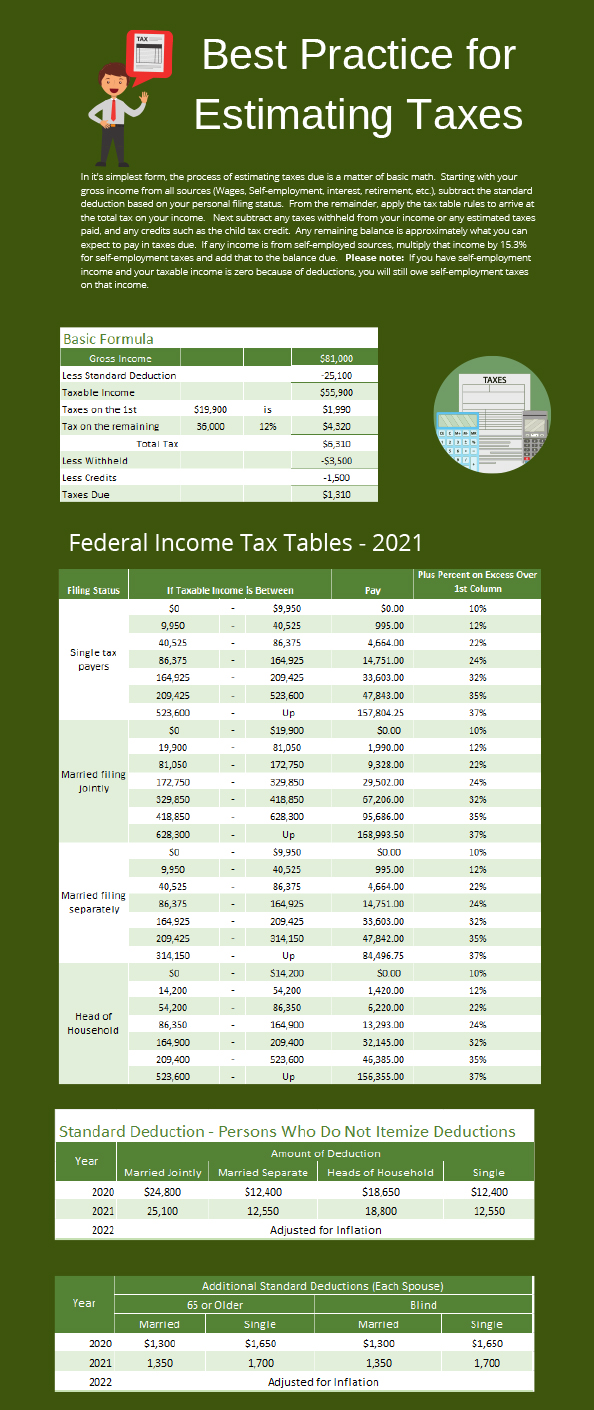

Step One: Starting with your gross income from all sources (Wages, Self-employment, etc.) subtract the standard deduction based on your personal filing status.

Step Two: From the remainder, apply the tax table rules to arrive at the total tax on your income.

Step Three: Next subtract any taxes withheld from your income (W2, and prior estimates) and any credits such as the child tax credit. Any remaining balance is approximately what you can expect to pay in taxes due.

Step Four: If any of your income is from self-employed sources, multiply that net income by 15.3% (.153) for self-employment taxes and add that to the balance due.

Step Five: Divide the total balance into 4 payments and make the first payment by April 18th. You can find forms and worksheets here and at IRS.gov.

We’ve created some examples and tables for you on an infographic that can be found here on our website. If you work with a tax preparer each year, you can usually ask them to produce the estimates for you along with the forms. If you don’t have a tax preparer and need assistance, give us a call at (720) 924-3727 or schedule an appointment. We’re happy to help.